December Smart Strategies to Save and Invest for Retirement

December 2025

At the crest of wealth and wisdom

Retirement

Your Guide to Building a Secure Financial Future

Welcome to This Month’s Retirement Planning Newsletter!

Retirement may seem far away to some of you, but the earlier you start saving and investing, the better prepared you’ll be to enjoy your golden years. In this edition, we’ll explore practical ways to save and invest for retirement, tips to maximize your returns, and the importance of thoughtful planning as we close out the 2025 year.

1. Start Early and Stay Consistent

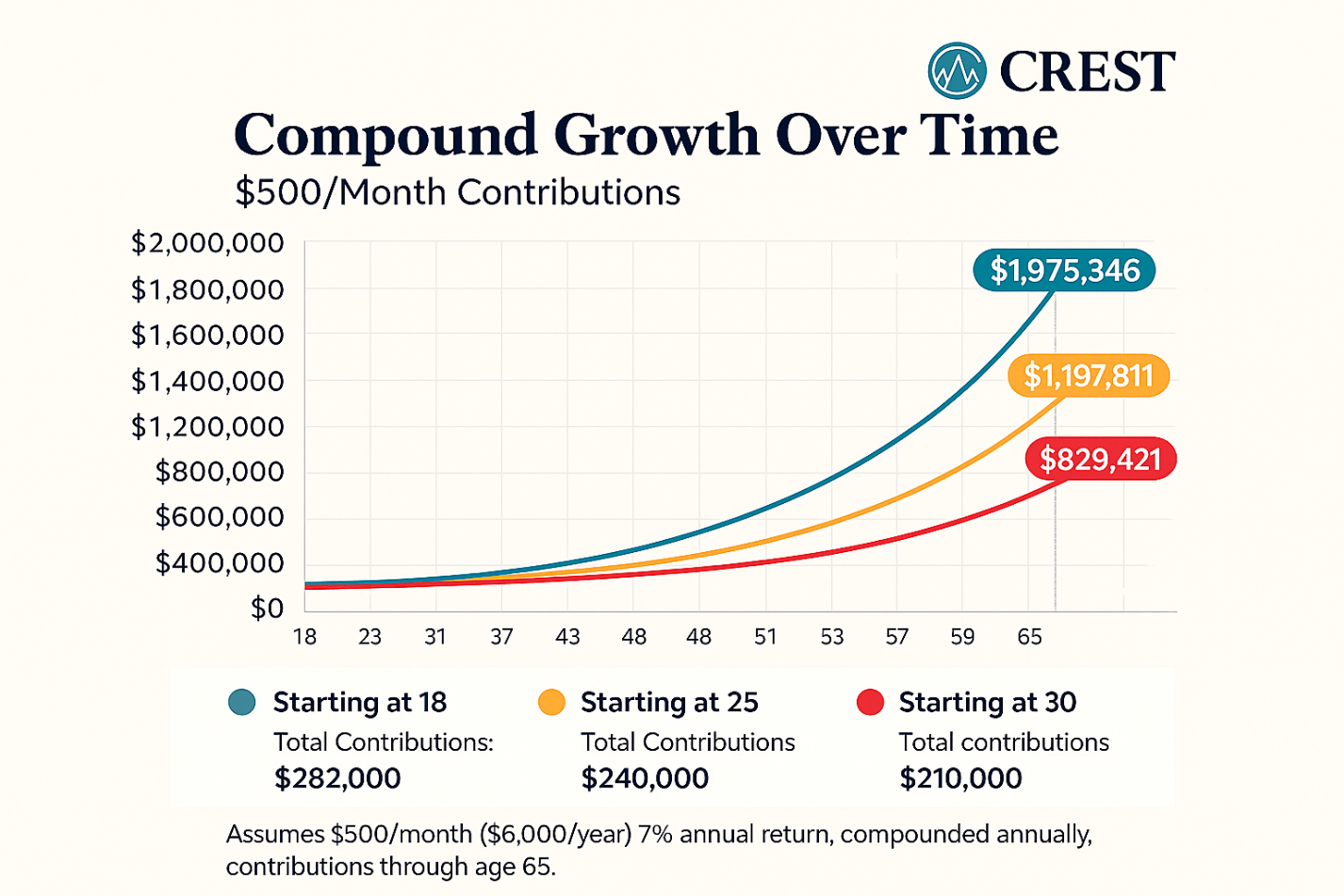

Time is one of your greatest allies when it comes to retirement savings. The sooner you begin saving, the more you benefit from compound interest—a powerful force that helps your money grow faster over time. Even small, regular contributions can accumulate into a substantial nest egg if you stay consistent.

While saving more later in life can be a great additional step, especially after getting important life events behind you, the time you need to grow and compound those savings becomes limited. Those dollars also run the risk of being moved into safer investments as you prepare for retirement to protect and preserve your nest egg. Retirement assets can become impacted by turbulent market events and the last thing you want is a bear market to come eat your savings right after you decide to stop working and nestle away more than normal. The sooner you can save and the more time you have to compound will benefit you in the long-run.

Even if you’re starting with a small amount each month it can benefit you in times of market stress to stretch yourself to save more during those years. Every 20%+ correction in markets has proven to be a buying opportunity. The average "garden-variety" bear market sees a 33% decline and takes around 21 months to recover to breakeven. Standard corrections typically recover in about four months. If you are buying on those dips you’re going to get ahead faster. Consistency is the key.

2. Make the Most of Employer-Sponsored Retirement Plans

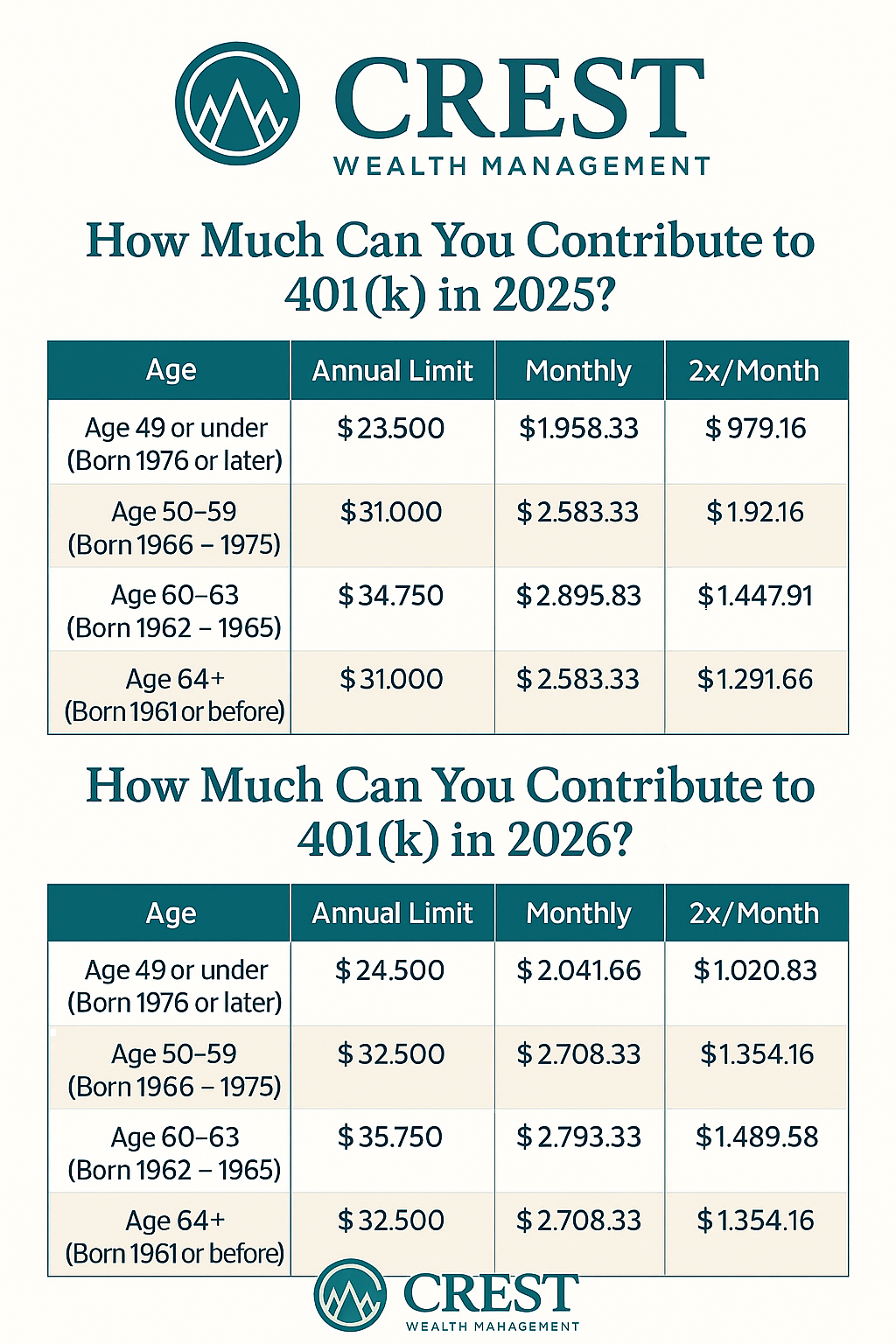

Many employers offer retirement plans such as 401(k)s or 403(b)s. These plans allow you to contribute pre-tax income, lowering your taxable income today while building wealth for tomorrow. Be sure to contribute at least enough to take full advantage of any employer matching contributions—this is essentially free money!

You can also make after-tax contributions if your plan allows it, which puts you in a position to save even more money within your 401(k) or 403(b) plan. The total Employee + Employer contributions allowed are $70,000 for 2025 and $72,000 for 2026. For example, if you're under 50 and contributing $24,500 and your employer is contributing $20,000 in 2026, you could contribute up to an additional $27,500 as after-tax contributions to bring your total to $72,000. There is a chance that your plan may not allow for these after-tax contributions, but that is where we can help by calling the plan administrator and helping you navigate this to ensure you’re maximizing your retirement savings.

3. Open and Fund an Individual Retirement Account (IRA)

An IRA is a personal retirement account that comes in two main forms: Traditional and Roth. With a Traditional IRA, your contributions may be tax-deductible, though withdrawals in retirement are taxable. A Roth IRA offers tax-free withdrawals in retirement, though contributions are made with after-tax dollars. Consider your current and expected future tax brackets when choosing between them; however, if you were to stay in the same tax bracket your entire life there is no difference, therefore having a retirement plan in place is an important step to model out your income needs and potential tax brackets in retirement so you can make the correct assessment.

IRA Contributions can be made up until April 15th for the prior tax year. This way you can always wait to assess your yearly income and tax situation before contributing. You will need to keep a few variables in mind such as if your covered by an employer plan, or what your household income is, to qualify for tax deductions on Traditional IRA contributions.

4. Automate Your Savings

Set up automatic transfers from your checking account to your retirement or investment accounts. Automating your savings helps you stay disciplined and reduces the temptation to skip contributions—even when life gets busy. This also allows you to dollar cost average into core positions in your portfolio through time and smooth out the volatility of markets.

The easiest step for automation is your employer 401(k), but it shouldn’t stop there. The next place would be your own IRA accounts, HSAs for medical and healthcare, and any excess savings can be deposited into a taxable brokerage account.

If you have high interest debt such as credit cards or loans, these should be paid down first. Always look at if the interest you’re being charged on debt is higher than the annual return you can likely earn in your investments. If it is, pay down the debt first.

5. Diversify Your Investments

Don’t put all your eggs in one basket. There is a saying that “Concentration builds wealth, Diversification keeps it.” Earlier in life you can afford to concentrate you wealth in fewer investments, however, if you are investing for an approaching retirement date, it is important to spread your investments among stocks, bonds, cash, real estate, precious metals, mutual funds, and other asset classes to help reduce risk and improve your odds for steady growth. As you get closer to retirement, consider shifting to more conservative options to preserve your capital in alignment with your financial plan while still maintain an agreed element of growth to fight inflation.

6. Monitor and Adjust Your Plan

Review your retirement savings strategy at least once a year. Life changes, market conditions shift, and your goals may evolve. Make adjustments as needed to stay on track for your target retirement age and lifestyle. This is becoming ever more important with government policy changes, tax laws, higher inflation, and global monetary system shifts.

7. Avoid Common Pitfalls

· Don’t cash out retirement accounts early—this often comes with 10% penalties, tax implications, and lost growth opportunities.

· Watch out for high fund fess, and account fees that can eat into your savings over time.

· Resist the urge to make impulsive investment decisions based on market swings like we have seen in 2025. There is no need to be overly nervous if you have set money aside for short-term needs such as the next 6-12-18 months.

· Avoid commonplace thinking of what worked the past 40 years will continue to work in today’s environment. Be willing to change your investment strategy when new information comes to the surface.

· Lifestyle creep can leave us with larger bills and less disposable money to invest. It happens to all of us as we grow our careers and family, but there is a cost to it on the backend when it comes to retirement savings if you are not buying productive assets/income streams that can help you in the future.

8. Seek Professional Guidance

A financial advisor can help you create a personalized retirement plan, select the right investment options, and navigate complex financial decisions. Their expertise can help you feel confident about your long-term strategy. We are not just saying this because this is what we do for a living. I can’t tell you the amount of times we have seen people leaving meaningful interest on the table with cash at the bank out of indifference, duplicating investments across multiple mutual funds creating concentration risk, using investment products without the proper context or consideration for taxes, and waiting to invest on a pullback that never comes.

Final Thoughts

Saving and investing for retirement is a journey, not a sprint. By starting early, making informed choices, and staying committed, you can build the financial security you deserve. Remember—every step you take today brings you closer to a comfortable and fulfilling retirement.

Ready to take control of your future? Start saving and investing for retirement today!

Disclosures:

Crest Wealth Management LLC is a registered investment adviser. Information presented is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Investments involve risk and, unless otherwise stated, are not guaranteed. Be sure to first consult with a qualified financial adviser and/or tax professional before implementing any strategy discussed herein. Past performance is not indicative of future performance.

Crest Wealth Management LLC may discuss and display, charts, graphs, formulas which are not intended to be used by themselves to determine which securities to buy or sell, or when to buy or sell them. Such charts and graphs offer limited information and should not be used on their own to make investment decisions.